What is LM test autocorrelation?

Background. The Breusch–Godfrey test is a test for autocorrelation in the errors in a regression model. The null hypothesis is that there is no serial correlation of any order up to p. Because the test is based on the idea of Lagrange multiplier testing, it is sometimes referred to as an LM test for serial correlation.

Is Durbin Watson test linked to residuals?

What is The Durbin Watson Test? The Durbin Watson Test is a measure of autocorrelation (also called serial correlation) in residuals from regression analysis. Autocorrelation is the similarity of a time series over successive time intervals.

What is the arch LM test?

The Lagrange multiplier (LM) test for autoregressive conditional heteroskedasticity (ARCH) of Engle (1982) is widely used as a specification test in univariate time series models. It is a test of no conditional heteroskedasticity against an ARCH model.

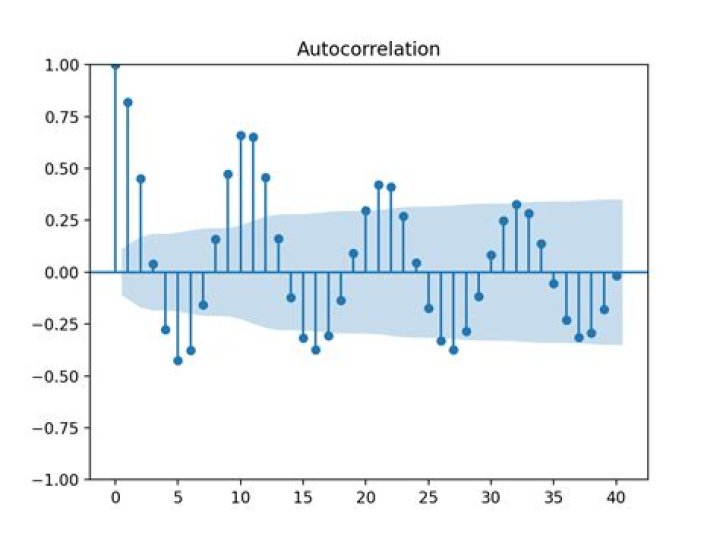

How do you test for serial autocorrelation?

You can test for autocorrelation with:

- A plot of residuals. Plot et against t and look for clusters of successive residuals on one side of the zero line.

- A Durbin-Watson test.

- A Lagrange Multiplier Test.

- Ljung Box Test.

- A correlogram.

- The Moran’s I statistic, which is similar to a correlation coefficient.

What is the difference between the breusch Godfrey test and the Durbin-Watson test?

Whereas the Durbin-Watson Test is restricted to detecting first-order autoregression, the Breusch-Godfrey (BG) Test can detect autocorrelation up to any predesignated order p. It also supports a broader class of regressors (e.g. models of the form yi = axi + byi-1 + c).

What is K in Durbin Watson?

In the following tables, n is the sample size and k is the number of independent variables.

How do you test the ARCH effect in EViews?

To test whether there any remaining ARCH effects in the residuals, select View/Residual Diagnostics/ARCH LM Test… and specify the order to test. EViews will open the general Heteroskedasticity Tests dialog opened to the ARCH page. Enter “7” in the dialog for the number of lags and click on OK.

How do you test the ARCH effect?

Engle’s ARCH test is a Lagrange multiplier test to assess the significance of ARCH effects [1]. y t = μ t + ε t , where μ t is the conditional mean of the process, and ε t is an innovation process with mean zero. for all lags h ≠ 0 and the innovations are uncorrelated.

What is Cochrane Orcutt iterative procedure?

Cochrane–Orcutt estimation is a procedure in econometrics, which adjusts a linear model for serial correlation in the error term. Developed in the 1940s, it is named after statisticians Donald Cochrane and Guy Orcutt.