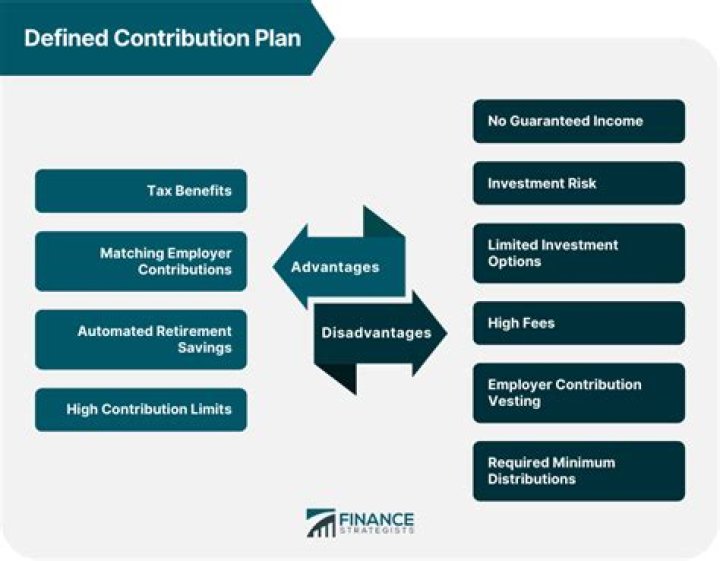

What is the difference between a defined contribution pension plan and a defined benefit plan?

A defined-contribution plan allows employees and employers (if they choose) to contribute and invest funds to save for retirement, while a defined-benefit plan provides a specified payment amount in retirement. These crucial differences determine whether the employer or employee bears the investment risks.

Which pension is better defined benefit or defined contribution?

Defined benefit pension This is also known as a career average pension or final salary pension, and is usually a better pension type compared to a defined contribution scheme, as it guarantees a set income when you retire.

How does a defined benefit pension plan work?

In a defined benefit pension plan, your employer promises to pay you a regular income after you retire. The income you get when you retire is usually calculated based on your salary and the number of years you contributed to the plan. It’s a set amount that does not depend on how well the investments perform.

What is a defined benefit plan example?

A defined benefit plan promises a specified monthly benefit at retirement. The plan may state this promised benefit as an exact dollar amount, such as $100 per month at retirement. Examples of defined contribution plans include 401(k) plans, 403(b) plans, employee stock ownership plans, and profit-sharing plans.

Is a defined benefit pension the same as final salary?

Defined benefit pensions, also known as final salary pensions, are often regarded as the gold-standard for retirement savings.

What defined benefit scheme?

A defined benefit (DB) pension scheme is one where the amount you’re paid is based on how many years you’ve worked for your employer and the salary you’ve earned. They pay out a secure income for life which increases each year. You might have one if you’ve worked for a large employer or in the public sector.

Do defined benefit pensions still exist?

DB pensions are most often provided by the public sector (health, education etc) and government employers. Some private sector employers do still offer them, however. Historically they have been seen as a very attractive kind of pension.